|

|

|

|

|

| |

|

|

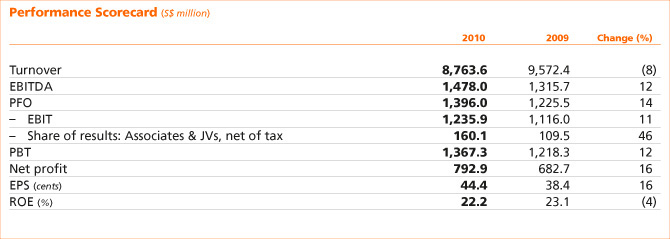

Sembcorp’s good performance in 2010 has

demonstrated the resilience of our strategy and

businesses. The Group’s net profit attributable to

shareholders of the Company (net profit) in 2010

grew by 16% to S$792.9 million, whilst turnover

was S$8.8 billion compared to S$9.6 billion in the

previous year.

During the year, the Group recorded an exceptional

gain of S$32.1 million comprising the Group’s share

of the Marine business’ full and final amicable

settlement of disputed foreign exchange transactions.

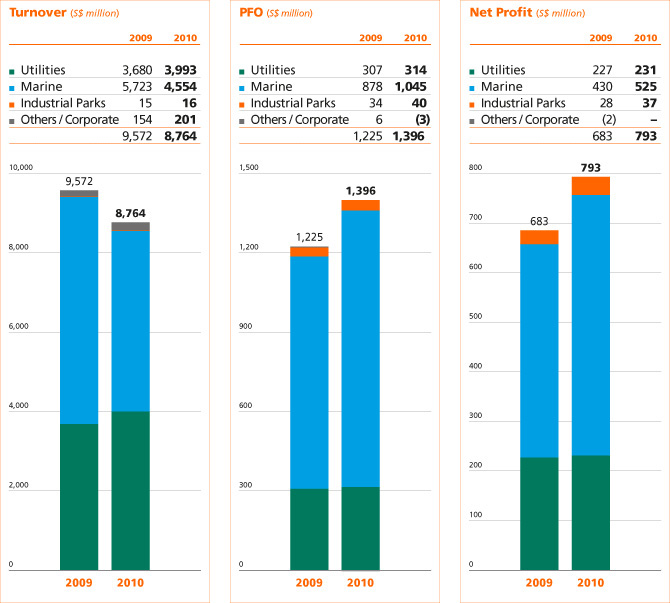

The Group achieved a turnover of S$8.8 billion,

with the Utilities and Marine businesses contributing

98% of total turnover.

The Utilities business’ turnover increased by 9%,

mainly due to higher high sulphur fuel oil (HSFO)

prices as well as the consolidation of Cascal’s turnover

with effect from July 2010.

The Marine business’ 2010 turnover decreased by

20% to S$4.6 billion mainly due to rig building as

well as offshore and conversion projects achieving a

lower percentage of completion revenue recognition

as compared to the prior year. There was also higher

variation order settlement for offshore contracts in

2009 as compared to 2010.

Revenue from the Others / Corporate segment

was mainly contributed by a subsidiary dealing

in specialised construction activities. The increase

in turnover in the segment compared to the year before was mainly due to differences in timing of the

recognition of revenue from projects.

The Group net profit in 2010 grew 16% from

S$682.7 million to S$792.9 million, while profit from

operations (PFO) increased 14% from S$1,225.5 million

to S$1,396.0 million.

The Utilities business’ net profit improved by 2% to

S$231.3 million. All regions registered growth except

for Teesside operations in the UK. Singapore operations

performed well, mainly driven by high electricity

prices and higher contribution from our natural gas

importation business. Outside Singapore, operations

in China and Middle East & Africa also registered

strong growth, increasing 226% and 80% respectively.

The performance of operations in Teesside, UK was

affected by lower volumes as a result of the previously

announced closure of some of its customers’ facilities,

low market spreads for power as well as the write-down

of certain ageing assets.

The increase in the Group’s share of the Marine

business’ 2010 net profit was mainly attributable to

the execution of projects ahead of schedule and the

achievement of better margins for the business’ rig

building, offshore and conversion projects through

higher productivity, as well as the resumption of

margin recognition for a rig building project upon

securing a buyer.

The Industrial Parks business’ higher net profit in

2010 was driven by healthy take-up for industrial,

commercial and residential land in its Vietnam industrial parks as well as improved contribution from

the business’ associate, Gallant Venture.

The exceptional item in 2010 relates to the Marine

business’ full and final amicable settlement of disputed

foreign exchange transactions. |

| |

|

|

As at December 31, 2010, the Group had cash and

cash equivalents of S$3.5 billion.

Cash flows from operating activities before changes in working capital increased from S$1,355.6 million

in 2009 to S$1,440.2 million in 2010. Net cash inflow

from operating activities for 2010 increased to

S$1,702.4 million, mainly due to receipts from ongoing

and completed projects.

Net cash outflow from investing activities for 2010

was S$761.4 million. S$632.3 million was spent on

expansion and operational capital expenditure and

S$18.8 million was for equity interests in an associate

and joint ventures. S$197.0 million (net of cash acquired) was spent for the acquisition of a 92.26%

equity interest in Cascal and S$15.8 million for an

additional 5.4% equity interest in Cascal. The above

cash outflows were partially offset by dividends and

interest received of S$97.3 million.

The net cash outflow from financing activities

of S$29.5 million in 2010 related mainly to dividends

and interest paid, partially offset by net proceeds

from borrowings.

During the financial year, the Company issued

3,630,192 new ordinary shares amounting to

S$17.1 million for the acquisition of all remaining

shares in The China Water Company (CWC) not already

held by its municipal water subsidiary Cascal from

Waterloo Industrial, CWC’s only other shareholder.

Group shareholders’ funds increased from

S$3.3 billion at December 31, 2009 to S$3.8 billion

at December 31, 2010. The decrease in ’Other reserves’

was mainly due to foreign currency translation loss;

partially offset by fair value gain on Cosco Corporation

(Singapore) (Cosco) shares held by the Marine business.

Non-current assets, with the exception of

investment properties, increased primarily due to the

consolidation of Cascal. ’Interests in associates’ and

’Interests in joint ventures’ increased due to higher

contributions recorded in 2010. Intangible assets

include goodwill as well as intangible assets arising

from service concession agreements. ’Other financial

assets’ increased, mainly due to fair value adjustments

of Cosco shares held by the Marine business.

’Inventories and work-in-progress’ decreased

and ’Cash and cash equivalents’ increased, mainly

due to receipts from the Marine business’ completed

rig building projects. ’Assets held for sale’ mainly

relates to the disposal of property, plant and

equipment (PPE) by the Utilities business. ’Deferred tax

liabilities’ increased mainly due to the consolidation of

Cascal. Increase in ’Provisions’ was mainly due to higher

provision for restoration of PPE by the Marine business.

’Interest-bearing borrowings’ increased primarily due

to medium-term notes issued by the Group’s wholly-owned

treasury subsidiary, Sembcorp Financial Services

(SFS), increased bank borrowings for the acquisition

of Cascal and funding of Utilities operations, mainly in

Oman. The increase in ’Other long-term liabilities’ was

mainly due to an amount owed to a non-controlling interest of a subsidiary as well as the consolidation

of Cascal.

Return on equity (ROE) for the Group was a healthy

22.2% in 2010 and earnings per share (EPS) increased

to 44.4 cents.

Subject to approval by shareholders at the next

annual general meeting, a final tax exempt one-tier

dividend of 17.0 cents per ordinary share comprising a

final ordinary dividend of 15 cents per ordinary share

and a final bonus dividend of 2 cents per ordinary

share has been proposed for the financial year ended

December 31, 2010.

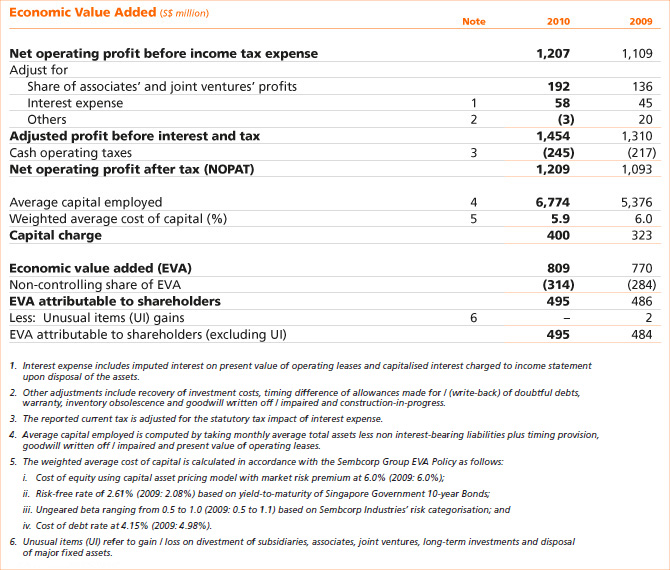

The Group generated positive economic value

added (EVA) of S$809.4 million in 2010. This positive

EVA creation was mainly driven by better Group earnings.

Our net operating profit after tax (NOPAT) for 2010

amounted to S$1.2 billion whilst capital charges increased

to S$399.6 million, mainly due to a higher capital base.

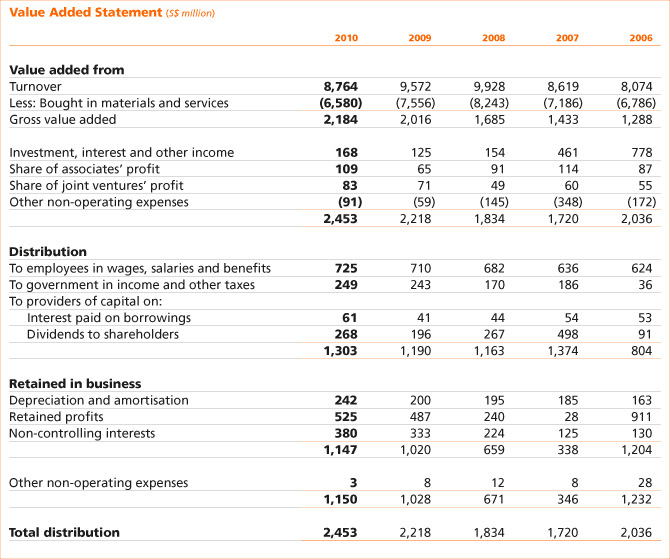

In 2010, the Group’s total value added was

S$2.5 billion. This was absorbed by employees

in wages, salaries and benefits of S$724.9 million,

by governments in income and other taxes of

S$248.6 million and by providers of capital in interest

and dividends of S$328.7 million, leaving a balance

of S$1.2 billion reinvested in business.

Sembcorp’s financial statements are prepared

in accordance with Singapore Financial Reporting

Standards (FRS).

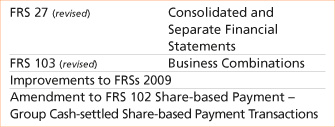

With effect from January 1, 2010, the Group adopted

the following new / amended FRS and Interpretations

of Financial Reporting Standards (INT FRS): |

| |

|

| |

The adoption of the above FRS (including

consequential amendments) does not have any

significant impact on the Group’s financial statements,

except for the impact of FRS 103 and FRS 27 as

indicated below.

The revised FRS 103 introduces a number of

changes in accounting for business combinations

occurring after July 1, 2009. These changes will impact

the amount of goodwill recognised, the reported

results in the period that an acquisition occurs, and

future reported results. The Amendments to FRS 27

require that a change in the ownership interest of a subsidiary (without loss of control) is accounted

for as an equity transaction. Therefore, such

transactions will no longer give rise to goodwill,

nor will they give rise to a gain or loss. Furthermore,

the amended standard changes the accounting

for losses incurred by the subsidiary whereby

losses applicable to the non-controlling interests

in a subsidiary are allocated to the non-controlling

interests, even if doing so causes the non-controlling

interests to have a deficit balance. These changes

in the revised FRS 103 and Amendments to

FRS 27 will affect accounting for acquisitions or loss of control and transactions involving non-controlling

interests.

The Group’s activities expose it to a variety of

financial risks, including changes in interest rates,

foreign exchange rates and commodity prices as

well as credit risk.

Please refer to the Risk Management & Mitigation

Strategies chapter of this report for details on the

management of these risks.

Sembcorp’s financing and treasury activities

continue to be mainly centralised within our wholly-owned subsidiary Sembcorp Financial Services (SFS),

the Group’s Treasury vehicle. SFS facilitates funding

and on-lends funds borrowed by it to the companies

within the Group, where appropriate.

SFS also actively manages the cash within the

Group by taking in surplus funds from those with

excess cash and lending to those with funding

requirements. We actively manage the Group’s excess

cash, deploying it to a number of financial institutions

and actively tracking developments in the global

banking sector. Such proactive cash management continues to be an efficient and cost-effective way

of managing the Group’s cash and financing its

funding requirements.

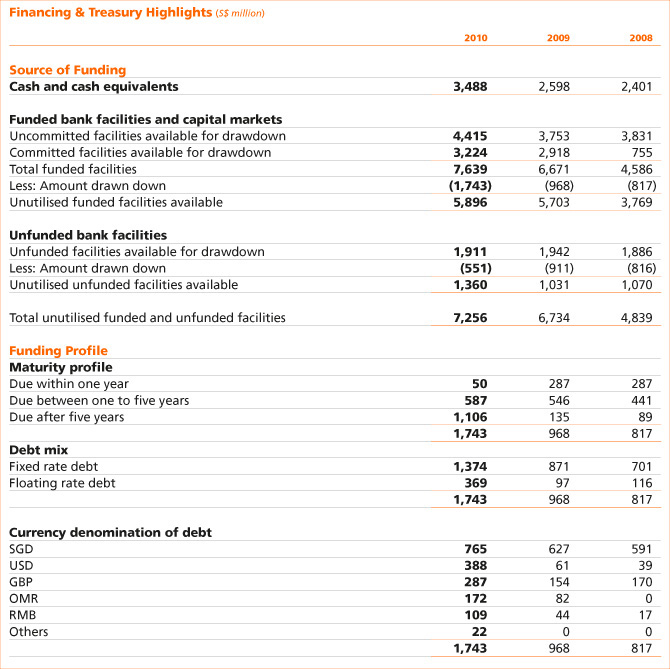

Including SFS’ S$1.5 billion and Sembcorp Marine’s

S$2 billion medium-term note programme, the Group’s

total funded facilities as at end 2010 amounted to

S$7.6 billion (2009: S$6.7 billion), with unfunded

facilities standing at S$1.9 billion (2009: S$1.9 billion).

While Europe and the USA have experienced a

slowdown in economic growth in the past year, Asia

has nonetheless continued to enjoy robust growth in

2010. Against this background, the market has seen

a substantial inflow of funds diverted towards Asia in

search of investment opportunities and high returns,

offering the Group the opportunity to tap funding

markets at a level almost comparable to the period

prior to the collapse of Lehman Brothers Holdings.

In 2010, the Group seized the opportunity to issue

a S$100 million 7-year note maturing in September

2017, a S$300 million 10-year note maturing in April

2020 and a S$100 million 15-year note maturing in

August 2025 under SFS’ S$1.5 billion medium-term

note programme. The Group aims to term out the

loans such that their maturity profile mirrors the life

of our core assets, while concurrently continuing

our focus on maintaining adequate liquidity for the

Group’s businesses.

We continue to build on our banking relationships

with a view to ensuring that when commercially viable

and strategically attractive opportunities arise, we are

able to secure funding on competitive terms.

The Group remains committed to balancing the

availability of funding and the cost of funding,

together with the need to maintain prudent financial

ratios. We also aim to maintain an efficient and optimal mix of committed and uncommitted facilities

and fixed and floating rate borrowings.

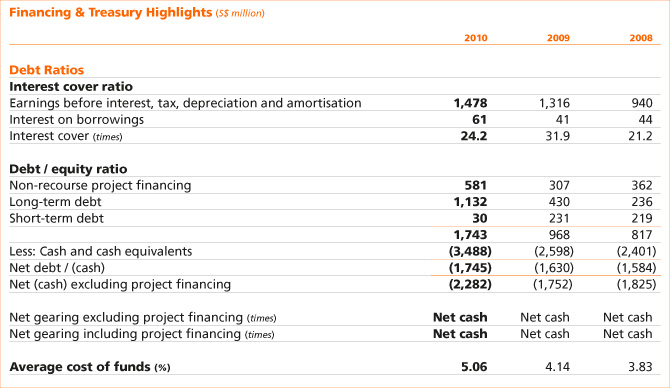

As at December 31, 2010, gross borrowings

amounted to S$1.7 billion (2009: S$967.7 million)

which was higher than last year. The incremental

borrowings were used to fund the Group’s new

projects and acquisitions. As the Group continues to

grow organically and inorganically, the Group will

also potentially tap new borrowings to fund its

growth. Of the overall debt portfolio, 79% (2009: 90%)

constituted fixed rate debts which were not exposed to

interest rate fluctuations.

The Group seeks to limit its interest rate exposure

by adopting a prudent debt structure, balancing this

with liquidity and cost considerations. The weighted

average cost of funding was 5.06% (2009: 4.14%)

which was higher than previous year due to the

terming out of the loans. The interest cover ratio is

still in a very healthy range. With the increase in gross

debt, this ratio was reduced to 24.2 times in 2010 as

compared to 31.9 times in 2009.

As at end 2010, the portion of the Group’s debt

maturing beyond one year was 97% (2009: 70%). Only

S$50.1 million of the Group’s debt is due within 12 months. |

| |

|

|

|

|